Futures Market: Overnight, LME copper opened at $9,619/mt, initially rose slightly before pulling back to a low of $9,608.5/mt, then fluctuated upward throughout the session, reaching a high of $9,679/mt near the close and finally settling at $9,679/mt, up 1.96%. Trading volume reached 18,000 lots, and open interest stood at 300,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened at 78,420 yuan/mt, fluctuated rangebound initially, dipped to a low of 78,270 yuan/mt, then climbed upward and fluctuated rangebound near the close, reaching a high of 78,600 yuan/mt and finally settling at 78,500 yuan/mt, up 0.91%. Trading volume reached 23,000 lots, and open interest stood at 157,000 lots.

【SMM Copper Morning Brief】News: (1) US Trade Policy - Trump threatened to impose a 50% tariff on all steel and aluminum products from Canada, aiming to destroy Canada's automotive industry through tariffs. In response, Ontario, Canada, suspended a 25% surcharge on electricity exports to the US. White House officials later announced the cancellation of the 50% tariff on Canadian steel and aluminum. This round of trade conflict between the two sides lasted approximately six hours.

(2) US January JOLTs job openings rose to 7.74 million, exceeding the expected 7.63 million. Subsequently, traders increased their bets on a US Fed interest rate cut.

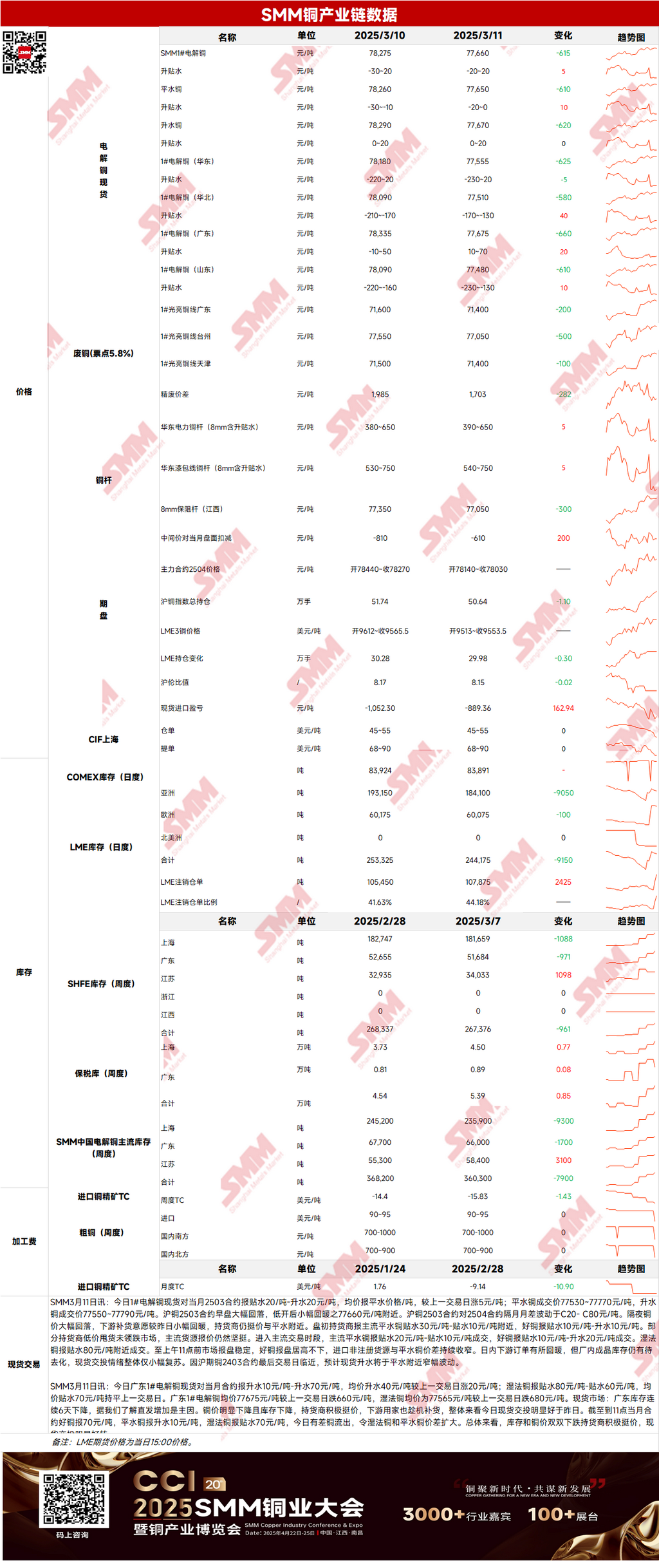

Spot Market: (1) Shanghai: On March 11, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 20 yuan/mt to a premium of 20 yuan/mt, with an average price at parity, up 5 yuan/mt from the previous trading day. Downstream orders slightly improved yesterday, but finished product inventories at plants still need to be reduced. Overall, spot trading sentiment only saw a slight recovery. As the last trading day of the SHFE copper 2403 contract approaches, spot premiums are expected to fluctuate rangebound near parity.

(2) Guangdong: On March 11, #1 copper cathode spot prices against the front-month contract were quoted at a premium of 10 yuan/mt to 70 yuan/mt, with an average premium of 40 yuan/mt, up 20 yuan/mt from the previous trading day. Overall, with both inventories and copper prices declining, suppliers stood firm on quotes, and spot trading improved significantly.

(3) Imported Copper: On March 11, warehouse warrant prices were $45-55/mt, QP March, with the average price unchanged from the previous trading day; B/L prices were $68-90/mt, QP April, with the average price unchanged; EQ copper (CIF B/L) was $10-20/mt, QP March, with the average price unchanged. Quotes referenced cargoes arriving in mid-to-late March and early April. Yesterday, the SHFE/LME price ratio for the SHFE copper 2503 contract was around -900 yuan/mt. LME copper 3M-Mar was at C$7.71/mt, LME copper 3M-Apr was at B$0.58/mt, and March-date to April-date was around C$8.29/mt. Although the price ratio improved yesterday, market trading sentiment remained subdued, with only a small volume of EQ and fire-refined warehouse warrants traded. Overall, trading activity was not active.

(4) Secondary Copper: On March 11, secondary copper raw material prices fell by 200 yuan/mt MoM. Guangdong bare bright copper prices were 71,300-71,500 yuan/mt, down 200 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,703 yuan/mt, down 282 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,130 yuan/mt. According to the SMM survey, secondary copper rod consumption in the Hebei market was sluggish, with many secondary copper rod traders reporting that inventories had returned to normal levels. Inventory is expected to continue decreasing before the end of this week.

(5) Inventory: On March 11, LME copper cathode inventories decreased by 9,150 mt to 244,175 mt. On March 11, SHFE warrant inventories decreased by 4,891 mt to 151,703 mt.

Prices: Macro side, Trump announced plans to double the 25% import tariff on Canadian metals, but White House officials later stated that this plan would not be implemented. Following the conflicting tariff news, market trading fluctuated, US stocks fell, and the US dollar index hit a new low, providing support for copper prices. Fundamentals side, copper prices pulled back from highs yesterday. Downstream orders slightly improved, and some companies reported a slight increase in purchasing demand. However, finished product inventories at plants remained high, and destocking pressure persisted. Spot market trading sentiment only saw a slight recovery, with traders and downstream companies mostly purchasing as needed. Overall, the market still faces a supply-demand imbalance. Copper prices have limited upside room but remain well-supported at the bottom.

》Click to View SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only and does not constitute direct investment research advice. Clients should make cautious decisions and not replace independent judgment with this information. Any decisions made by clients are unrelated to SMM.】